Equity for Product Managers

Cliffs, Liq Prefs, Share Classes and other terms you should know about

Introduction

“Read, and then sign,” lawyers say. But when you don’t understand the language, does reading the document help? Equity regulations differ from country to country, and seemingly all parameters can be adjusted (trust me, lawyers are creative). Most people are not finance experts, and will not invest enough time to understand all the intricacies of their equity contracts. After all, humans are satisficers - we settle for good enough options based on the limited data we have, rather than seeking the absolute best option.

Life is too short to know everything about equity.

With a background in biomedicine, I did not understand my first equity contract. Luckily, my hiring managers were experts in the field and gave me an intro. After all, I was signing a contract to become a Product Manager in an equity management startup. A couple of years later, I can understand even the most creative lawyers (JSOP creators, I am looking at you 🤓). Knowing how it is to be on both sides of knowledge, in this article I intend to explain equity in words that my past self would understand.

Chapter 1: Shares & share classes

Simply said, a share is a unit of ownership of the company. Collectively, shares are called stock. Some of the most important components of a share are monetary value and voting rights. And while both of these terms are self-explanatory, the devil is in the details.

Two individual shares in the same company might have completely different monetary values and voting strengths. When the company is first created, common or ordinary shares get issued. This share class is given to founders, employees, and early investors. In the following financing rounds, preferred share classes will be created (preferred A, preferred B,…). The terms of the share classes are negotiated between the new investors and the board. For example, 1 preferred A share might get 5 times more voting power than the common share. Or be served first in case of an exit (more on this in Chapter 3).

So if the stock were a cake, a share would be a slice of the cake. A small party requires a uniform 1-level Common Chocolate cake. As more attendees join, we cater to different preferences and create an Apricot cake, Banana cake, and Coconut cake (see what I did there? #soPunny 🥲). These are all added on top.

Equity is like a cake. As the party becomes bigger, new cakes are stacked on top of each other. From the outside, they might look the same, but each layer can be very different.

Chapter 2: Employee Equity

Grant allocation

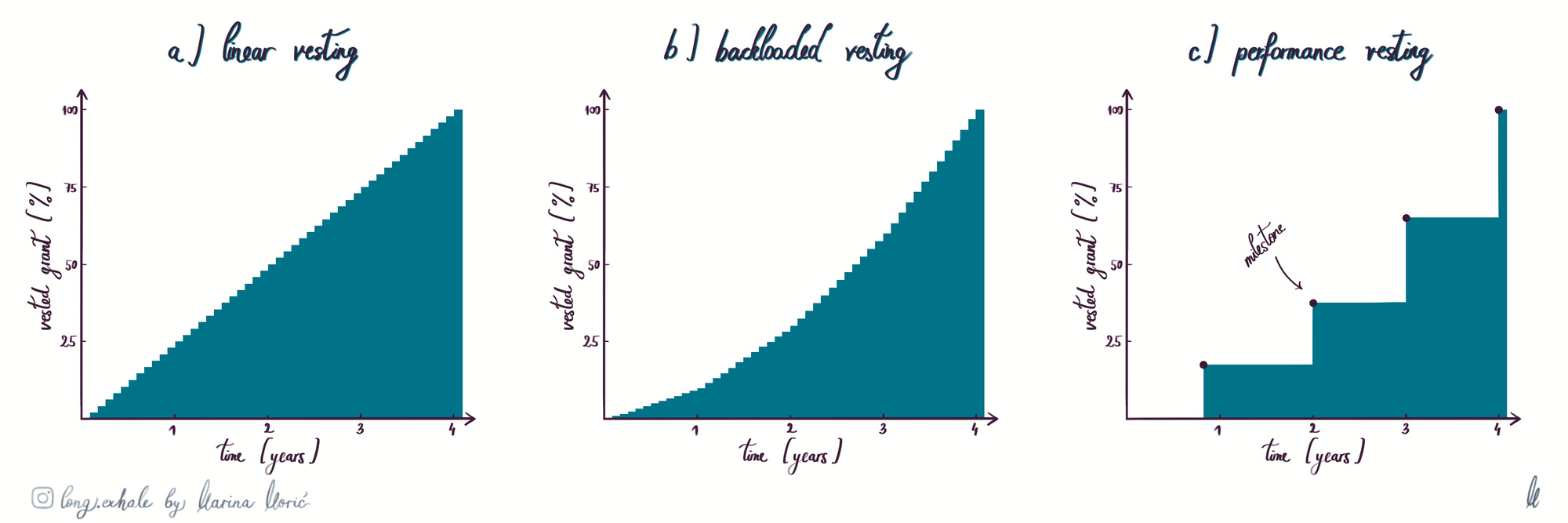

Around 10-20% of the company’s equity is put aside to attract and retain talent. This portion of the equity is called an employee equity pool, and the exact percentage is negotiated with the board. Equity is given to employees in the form of a grant, and the way in which equity is allocated over time is called vesting. There are many ways to set up vesting, but the three most talked about are linear, backloaded, and performance vesting.

Linear vesting is a time-based vesting in which an equal amount of equity is earned every month (or any other frequency as defined by the contract).

Backloaded vesting is a time-based vesting in which the earned amount is not always the same. In the beginning, employees earn a lower percentage of the grant, and more as the vesting progresses.

Performance vesting is milestone-based vesting in which one needs to reach a certain target or targets (usually within a certain time span) to earn equity.

Different ways to allocate equity over a 4-year period. While the X axis represents time in years, the Y axis is the percentage of the grant vested. a) Linear vesting: employee receives 25% of their grant each year. b) Backloaded vesting: the employee receives 10% of their grant in the first year, 20% in the second, 30% in the third, and 40% in the fourth. c) Performance vesting: The employee receives a contractually specified grant percentage if the target is reached in a specific time frame.

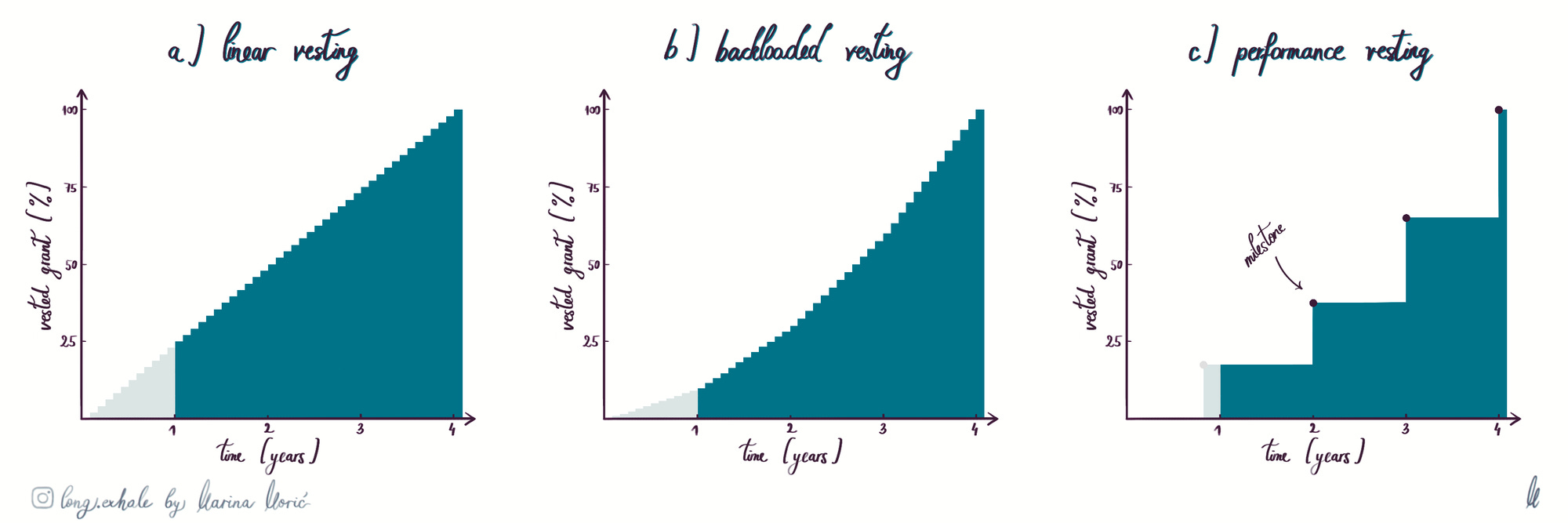

More often than not, vesting will start with a cliff. Cliff is a time period in which, if you leave, you are not entitled to any equity. This protects the company from employees who join startups to diversify their investment portfolio, improves employee retention, and makes reporting to authorities easier.

Grants tend to be given over a 4-year vesting period, which starts with a 1-year cliff. If this still sounds confusing, imagine we are talking about salaries. In most companies, salaries are expressed as yearly, pre-tax amounts. In equity words: 1-year linear vesting with no cliff, and monthly intervals. A bonus received as you reached a certain target would be an immediate, no cliff, performance vesting.

Three types of 4-year vesting with a 1-year cliff. The X axis is time in years, while the Y axis represents the percentage of the grant vested.

Grant types

Because of the potential high taxation, employees rarely receive issued shares. Most commonly, they will be given options, virtual (or phantom) shares, or forms of stock that postpone or reduce taxation (e.g. restricted stock units, hurdle shares, etc.). Describing all types of equity is out of the scope of this article, but let’s introduce options and phantoms. Bear in mind that there are no good or bad grant types, it all depends on the conditions that the company is setting (more on that in Chapter 3).

Options give employees the right (not obligation) to buy shares at a pre-defined (often discounted) rate. The action of buying these shares is called exercising, and the exercise price is commonly referred to as the strike price. You can exercise vested options when the company opens the exercising window. These open periodically (e.g. every year) or during specific events like funding rounds, termination of the contract, etc.

Phantom shares provide employees the economic benefit of owning a share, without giving them ownership rights over shares. In other words, phantom shares mimic the value of the share without giving you other benefits that shares might entail (e.g. voting rights, dividends). The payout is contractually defined and usually coincides with funding rounds or termination of the contract.

Chapter 3: Profitability

Value distribution

The way to get the value out of your shares is to sell them (Captain Obvious to the rescue). In public companies, this is done on a stock exchange, and while the company is still private, you can do it on secondary markets or through buyback. In most companies, both of these happen relatively rarely. Buyback is when a company buys the shares from the stakeholder, while in secondary events shares are offered to other stakeholders (i.e. share owners) in a specific order. Both of these require quite some effort, and many companies decide they are not worth the hassle. In that case, your only option to sell it is if the company is successful enough that it goes through an IPO (initial public offering) or it gets acquired by another company..

Value distribution at an exit is complex but I believe it is important to understand the basics. To make it a bit more tangible, I will explain it with an example. At the seed stage, you receive 10 000 shares at a price of 1 CHF per share. This represents 1% of the company, and you can easily calculate that the company has 1M shares and a valuation of 1M CHF. During Series A, the company created 0.25M shares for new investors and to top up the employee pool. You now own 0.8% of the company, and this reduction in your ownership percentage is called dilution. Most frequently, financing rounds dilute current shareholders by 10-30%. Let’s take 20% as an average. Without refresher grants (additional grants given to employees during promotions or similar), by Series B you are down to 0.64% ownership, and by Series C 0.512%. At this time, the company has almost 2M shares.

Now, there is another variable. Investing in startups is a risky business, and investors need one golden child that will turn enough profit to cover for the failing ones. Then again, the later you invest, the more you pay for the same percentage of ownership. These are some of the reasons liquidation preferences were invented. Stock with liquidation preference has the right to profit before common stakeholders, often by the “last come, first served” principle. In this case, profits would be first given to Preferred C, then Preferred B, then Preferred A, and only then to common shares (which are usually given to employees). Liquidation preference comes with a multiple - a factor by which preferred stockholders receive their investment. For example, a Series C investor that invested 1M CHF with a 3x multiple is entitled to 3M CHF before anyone else gets a payout.

Let’s go back to our cake analogy. Your invitation states you will get one piece of the bottom Chocolate cake. What you don’t know is that some people requested 2 pieces, otherwise, they will not show up. The cake will be given to these people first and cut from the top down. Whether you get your slice depends on the cake budget. And the main question is - would you join the party although you might not get the cake?

Equity is like a cake. When you start distributing it, you start with the cake that was added last.

Taxation

In the eyes of the law, at the moment the share is issued - it has value. Meaning that they get taxed although you might never be able to get any profit. Taxation differs from country to country and depends on your grant type. To get a taste of taxation, below is an introduction to the taxation of options in Switzerland, and EMI (Enterprise Management Incentive) in the UK. These are, in many ways, best-case scenarios for employees.

Options in Switzerland. 🇨🇭 In short, you are taxed at exercise (i.e. when you convert options to shares), depending on the difference between the strike price and the value per share at the moment you are exercising. There are usually no costs associated with granting or selling the shares. One of the best, if not the best deals you can have. Let’s break it down with some numbers.

You receive a grant of 10 000 options that vest over 4 years. The market price per share is 1 CHF. No taxation at this point.

After 4 years, you exercise options. Your strike price is 0.01 CHF per share (defined by the company), and the market value is 5 CHF per share (defined by the authorities). You need to pay a 100 CHF strike price (0.01 x 10 000), and the 49 900 CHF ((5-0.01) x 10 000) is your taxable income. Taxes will depend on many different parameters, but let’s say you need to pay 15 000 CHF for this event.

You hold shares for some years, the company goes IPO, and you open that tasty bottle of wine you bought in Georgia 🇬🇪. The price per share is 20 CHF, and you sell all 10 000 shares, paying no taxes and receiving 200 000 CHF. You might not be a millionaire, but 184 900 CHF (200 000 - 100 - 15 000) is a nice profit.

EMI (Enterprise Management Incentive) in the UK. 🇬🇧 EMI is one of the most tax-efficient equity type in the UK, specifically designed for smaller companies. You don’t need to pay taxes at the date of the grant. And if the strike price is the same as the actual market value at the date of grant, you are not taxed at exercising either. In addition, if you hold the shares for 2 years before selling them, you only pay 10% capital gains tax when these are sold. So let’s break it down with numbers.

You receive a grant of 10 000 EMI options that vest over 4 years. The market value per share is £1, and this will be the future strike price. No taxation at this point.

After 4 years, you exercise options. The market value is £5, and your strike price £1. Hence, you pay £10 000. An important thing to note here is that, in case you leave your job, you have 90 days to exercise options to be eligible for 10% capital gains when selling the shares later on. If you exercise after 90 days, you will need to pay 20% capital gains when selling shares.

You hold these shares for some years, the company goes IPO, and you open that tasty bottle of wine you bought in Georgia 🇬🇪. The price per share is £20, and you sell all 10 000 shares, receiving £200 000. Out of this, £19 000 goes for capital gain taxes ((200 000 - 10 000) x 0.1). You might not be a millionaire, but £171 000 (200 000 - 10 000 - 19 000) is a nice profit.

Two examples of how taxation might occur. While the X axis represents time in years, the Y axis is the total value of the grant (not only what is vested at the time). On the left is the example of options in Switzerland, and on the right EMI options in the UK. Both of these examples are in many ways best case scenarios for employees, and one should not expect the same outcome.

Terms and Conditions

Equity might come with a series of terms and conditions. Many of them are pretty straightforward, but some of them are just… nasty. So here are a couple of things to look into.

The bad leaver clause defines what happens in case you leave the company under certain unfavorable circumstances. Most companies are rational and will only label you a bad leaver in case of serious misconduct. However, in some companies, you will be labeled a bad leaver if you just leave. Make sure you understand what is the definition of a “bad leaver” in your contract.

Clawback provisions allow the company to recover granted equity or its value from an employee under specific circumstances (financial misconduct or ethical breach). They can be used to reclaim already vested or exercised equity.

Forfeiture conditions are circumstances under which an employee may lose their right to unvested equity or shares in the future. For example, leaving the company before vesting is fully completed, or not exercising the shares before the expiry date.

Some grant types will have an expiry date. When it comes to options, this would be the date until which you need to exercise your options. If you don’t do it, you lose the right to purchase the underlying shares.

With phantom grants, you are sometimes only entitled to value increase until you leave, i.e. you will not benefit from the value increase that happens after you leave the company. I personally don’t think this is very fair, as early employees set the foundation for future growth.

Some companies create share classes worth a fraction of the common share. Similarly, 1 share might be converted to 100 phantom shares. So although the share price goes from $2 to $20, your phantom only increased from $0.02 to $0.2.

Acceleration provisions can trigger early vesting in certain conditions like an IPO or acquisition. Basically, your grant vests earlier than defined by your vesting schedule. Cool, right? 🤩

Dividends are regular payments to shareholders when the company makes a profit. These are more common in public companies.

Chapter 4: Funding Rounds and Product Management

Even if your startup doesn’t offer equity compensation, understanding equity and financing rounds comes in handy. In many ways, the requirements for the following funding round dictate the product focus.

Pre-seed startups are usually funded by “angel” investors - friends, family, and early supporters of the idea. Often, one or more founders assume the position of a product specialist. Their task is to create a minimum viable product and demonstrate the feasibility of their idea.

Seed startups need to show product-market fit (PMF) to raise the next round. The target market should show interest in the product, and be willing to pay for its services. Less than 10% of seed startups raise Series A.

Series A startups begin to scale more aggressively by expanding to new markets, growing the customer base, and building a strong foundation for growth. Series A is usually led by a VC firm whose members become part of the board and can affect the product direction.

Series B startups are focused on market expansion and other growth initiatives. For example, they might expand internationally, launch new product lines, or focus on maximizing market share (capturing the largest possible portion of the available market).

Series C is very often the last stop before an IPO, and companies are focused on reaching market dominance and profitability. This might involve building a completely new product, expanding to other markets, acquiring underperforming competitors, optimizing operations etc.

Chapter 5: Key Takeaways

I understand that this is a lot of information, so here are things to look into before accepting an equity offering.

What type of equity are you receiving?

What types of benefits are you entitled to (e.g. voting rights, dividends…)?

How is that equity type taxed in your country of residence?

What other costs are associated with receiving the equity?

What is your vesting schedule? Is there a cliff?

What is the current value and percentage of your equity?

Taking into consideration anticipated dilution, how will the value change with future rounds?

What other terms and conditions apply (forfeiture conditions, expiration dates, drawback clauses…)?

Does the company offer secondary events or buyback programs?

Does the company offer refresher grants? In which conditions?

Conclusion

State of equity worldwide reminds me of products that, with the best intentions, turned into feature factories. The intention is usually to reduce the risks for the company, employees, and/or investors. And as new regulations emerge, new equity types are created to circumvent the risks. However, the documentation is poor, there is no stakeholder alignment, and the customer success team was never hired to start with. In addition, the product has a strange monetization model and might be retracted at any time.

But as a proud owner of some exercised grants (humble brag 🥁), I am a big believer. Sure, it might be an endowment effect (cognitive bias where people ascribe a higher value to objects and items they already possess) or some other bias, but I see a lot of value in it. Equity makes you feel included. It gives you a feeling of community, ownership, and responsibility. We are all in this together, as a team.

Thank you Catarina Martins Simões for proofreading. 💜 If you want to share feedback or have a chat about product, biotech, digital art, equity,… (or have a recommendation for a good dog-sitter around Zürich), feel free to hit me up on LinkedIn. Cheers! 🥂

About Marina Morić

They say: ‘Jack of all trades, master of none.’ Marina answers: ‘Challenge accepted.’ Following years in the biomedical industry and receiving a Ph.D. in neuroscience, Marina shifted lanes to become a product manager in one of the fastest-growing fin-tech startups in Switzerland. With a steep learning curve, she jumped from intern to senior and became an equity expert in record time. Currently, Marina is on a sabbatical and on the lookout for a product that provides value to researchers, health professionals, and/or patients.

| A guest post by

|